By Rupert Rowling and Heesu Lee

Oil fell below $50 a barrel in London for the first time since May 2009 amid speculation that U.S. inventories will increase, exacerbating a global supply glut that’s driven prices to a five-year low.

Brent futures dropped as much as 2.8 percent.Crude stockpiles in the world’s biggest consumer, already at the highest for the time of year in three decades, probably expanded by 700,000 barrels last week, a Bloomberg News survey showed before an Energy Information Administration report today. China, the second-largest oil user, won’t drive a market rebound in 2015 as its net imports will slow, according to Citigroup Inc.

Oil slumped by 48 percent last year, the most since the 2008 financial crisis, as the U.S. pumped at the fastest pace in more than three decades and the Organization of Petroleum Exporting Countries decided to maintain its output ceiling. The market’s oversupply may take “months or years” to be absorbed, United Arab Emirates Energy Minister Suhail Al Mazrouei said.

“The market is looking for the appropriate equilibrium level post OPEC’s decision to hand over control of the price back to market,”Harry Tchilinguirian, London-based head of commodity markets at BNP Paribas SA, said by e-mail. “It has not found it yet. The mood will probably remain negative today given the very large build in U.S. product inventories.”

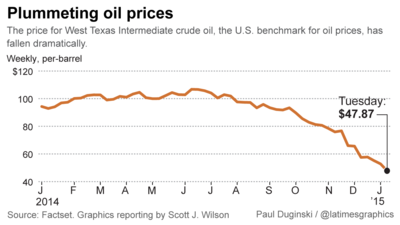

Brent for February settlement slid as much as $1.44 to $49.66 a barrel on the London-based ICE Futures Europe exchange, the lowest since April 2009, and was at $50.48 at 9:28 a.m. London time. The European benchmark crude traded at a premium of $3.04 to West Texas Intermediate.

U.S. Supplies

WTI for February delivery declined as much as $1.10, or 2.3 percent, to $46.83 a barrel in electronic trading on the New York Mercantile Exchange, the lowest since April 2009. The volume of all futures traded was 55 percent above the 100-day average for the time of day.

Implied volatility for at-the-money options in the front-month WTI contract rose to 60.2 percent this week, the highest level in more than three years, data compiled by Bloomberg show. It’s about 58 percent today, while Brent’s volatility is almost 49 percent.

U.S. crude inventories probably climbed to 386.2 million barrels in the week ended Jan. 2, according to the median estimate in the Bloomberg survey of nine analysts before the Energy Information Administration’s weekly report today. Supplies in the previous period were about 12 percent above the five-year average level for this time of year.

Chinese Imports

Distillate stockpiles, including heating oil and diesel, are projected to have gained by 1.75 million barrels, the survey shows, while gasoline supplies may have climbed 4.5 million.

Supplies at Cushing, Oklahoma, the delivery point for WTI contracts and the biggest U.S. oil-storage hub, gained by 482,000 barrels last week, the American Petroleum Institute said, according to a Twitter posting by Dominick Chirichella, a founding partner of Energy Management Institute in New York. Crude stockpiles nationwide shrank by 4 million, the industry group in Washington reported, according to the posts.

China’s net oil imports will probably rise 3.3 percent this year, compared with 8.9 percent in 2014, as “a slower build-out of refining capacity and record commercial storage builds in 2014 are likely to limit growth,” Citigroup strategists including Ivan Szpakowski in Hong Kong said in a research note.

‘Needs Time’

Oil’s oversupply “needs time to be absorbed” and prices this year may depend on output growth from non-OPEC producers, the U.A.E.’s Al Mazrouei said, according to The National, an Abu Dhabi daily. Qatar, another of OPEC’s 12 members, has estimated the global surplus at 2 million barrels a day.

Iran has held talks with Russia to reduce supply from the world’s biggest producer, according to Iranian Oil Minister Bijan Namdar Zanganeh. The parties haven’t reached a conclusion yet, the minister was cited by state-run Mehr news agency as saying.

While consensus within OPEC to stop the price decline is important, an emergency meeting of the group “won’t in itself solve problems,” Zanganeh said.

OPEC, which pumps about 40 percent of the world’s oil, agreed to maintain its output quota at 30 million barrels a day at a Nov. 27 gathering. It’s next scheduled to meet on June 5.

Los Angeles Times: 07. January 2015

Dark side of declining oil prices is economic pain for some countries

By CAROL J. WILLIAMS

Soaring demand from China kept oil prices above $100 a barrel for most of the last five years, but as growth slows there and elsewhere, the world is now awash in oil and its price has plummeted to less than $50 a barrel.

Here is a look at the consequences for some of the biggest producers:

RUSSIA: The oil-dependent economy has taken the biggest hit as Russia's national budget, which depends on energy sales for at least 60% of its revenue, has suffered the coinciding pain of U.S. and European Union sanctions for its aggression in Ukraine. With the per-barrel price now less than half what Kremlin budgeters forecast, the ruble has collapsed, causing prices to skyrocket for imported food and consumer goods. Tight money supply resulting from sanctions and shrinking currency reserves prompted the Russian Central Bank to raise interest rates to a whopping 17% in mid-December. Energy industry joint ventures have been suspended by the sanctions, and dozens of private businesses in thriving sectors like tourism have folded due to rising costs and dwindling clientele. President Vladimir Putin's lieutenants have accused the United States and Saudi Arabia of conspiring to keep oil prices low to inflict maximum damage on Russia and Iran. White House Council of Economic Advisors Chairman Jason Furman said on Dec. 16 that sanctions and the oil price fall have placed Russia "between a rock and a hard place in economy policy."

IRAN: A founding member of the Organization of the Petroleum Exporting Countries, Iran is losing about $2.5 billion a month due to falling oil prices, economist Saeed Laylaz told The Times on Tuesday. That will trim at least $30 billion from national income in 2015, he said, forcing the government to postpone vital public works projects and contributing to a jobless rate already over 30% for skilled labor. Oil sales are expected to account for about 25% of projected revenue for this year of $100 billion. That reflects a shortfall of about $50 billion from the government projects budgeted during last year's periodic optimism that a nuclear deal would be reached between Tehran and six world powers. Though the oil price drop has complicated relations between conservative Islamic clerical leaders and officials who support opening the state-dominated economy, slumping oil revenue could step up the pressure to renounce nuclear weapons production in exchange for sanctions relief.

VENEZUELA: Dependent on oil for 95% of its revenue, Venezuela is suffering one of the most profound economic contractions as a result of falling oil prices. President Nicolas Maduro has embarked on a global tour to drum up cash to keep the economy afloat as the price of its national crude has dropped to just above $47 a barrel, less than half of the $97.31 average of a little more than a year ago. He traveled to Moscow on Monday and will visit China, the source of most of its recent borrowing and destination of about a quarter of its 2.5 million barrels of daily oil exports. Maduro will also visit OPEC countries Saudi Arabia, Iran and Algeria. Maduro's predecessor, the late Hugo Chavez, built his populist following through hefty spending on projects aimed at lifting up the poor. Political discord, a history of nationalizing foreign assets and double-digit inflation have discouraged outside investment in modernization to lower the cost of production. Venezuela is already carrying $50 billion in debt to China, and the tumbling income from oil sales has stirred fear that the country will default on its foreign debt. Given those challenges, the outlook for the country weathering a long-running price slump is grim.

SAUDI ARABIA: Persian Gulf area oil producers have deep currency reserves to tide them over during the current price dive. Saudi Arabia has amassed $750 billion in hard currency reserves, says a Monday report by Forbes, providing it with a cushion to outlast competitors pushing for production cuts. In the 1980s, Saudi oil strategists saw that cutting output without like action by non-OPEC producers decreased market share before prices stabilized, Forbes noted. With major non-OPEC producers like Russia and Mexico unwilling to cut back and eliminate the glut, the Saudis have apparently calculated that they can outlast the competition and preserve their market domination.

CANADA: Eroding per-barrel prices portend trouble for Canada's industry as production costs are high from its oil and tar sands sources. Oil and gas and their related industries account for about 11% of Canada's GDP, the Royal Bank of Canada said in a report issued Monday, and the industry's heavy concentration in Alberta will hit the economy of that western province. The drop in oil prices is likely to have its greatest effect on investment in extraction, which drew more than $90 billion to Canada in 2013, the RBC reported. But Natural Resources Canada, a government resource, predicts the country will benefit as a whole from the lower prices for fuel for citizens, public transportation and fuel-intensive industries, more than offsetting the investment losses. And the RBC said the drop in gasoline prices in the United States, Canada's No. 1 export market, would free up cash for consumers to buy more Canadian goods.

MEXICO: The oil price tumble complicates Mexico's ambitious attempt to attract foreign investment as it privatizes the Pemex energy behemoth. Mexico has already drawn China into $19 billion worth of energy and infrastructure collaboration aimed at reducing its reliance on the United States, which buys 80% of Mexican exports. Like Canada and Brazil, Mexico has a more diversified economy than other major oil producers and may be able to weather the price drop long enough to convince potential investors that development opportunities will outlive the crisis. But slow progress in reforming the sector and tax increases last year prompted the Mexican government to lower its 2014 growth forecast to 2.5% from 3.9%.

UNITED STATES: As the world leader in natural gas production from its booming shale fields, the U.S. can expect a boost in consumer spending from drivers' savings on gasoline. But as economists worldwide point out, drains on the economies of countries that are major importers of U.S. goods may herald a slump in exports as trading partners tighten their belts. "Falling prices at the pump benefit consumers and the specter of inflation is being held at bay," the Gulf News oil analyst observed in a commentary last month. "But U.S. authorities are taking a very short-term view. Should cheap oil hit the economies of America's trading partners in a major way, U.S. exporters will feel the pinch and jobs will be lost."

No comments:

Post a Comment